Television broadcasting and production company AMC Networks (NASDAQ:AMCX) reported Q3 CY2025 results exceeding the market’s revenue expectations, but sales fell by 6.3% year on year to $561.7 million. Its non-GAAP profit of $0.18 per share was 47.4% below analysts’ consensus estimates.

Is now the time to buy AMC Networks? Find out by accessing our full research report, it’s free for active Edge members.

AMC Networks (AMCX) Q3 CY2025 Highlights:

- Revenue: $561.7 million vs analyst estimates of $547.2 million (6.3% year-on-year decline, 2.7% beat)

- Adjusted EPS: $0.18 vs analyst expectations of $0.34 (47.4% miss)

- Adjusted EBITDA: $82.92 million vs analyst estimates of $74.71 million (14.8% margin, 11% beat)

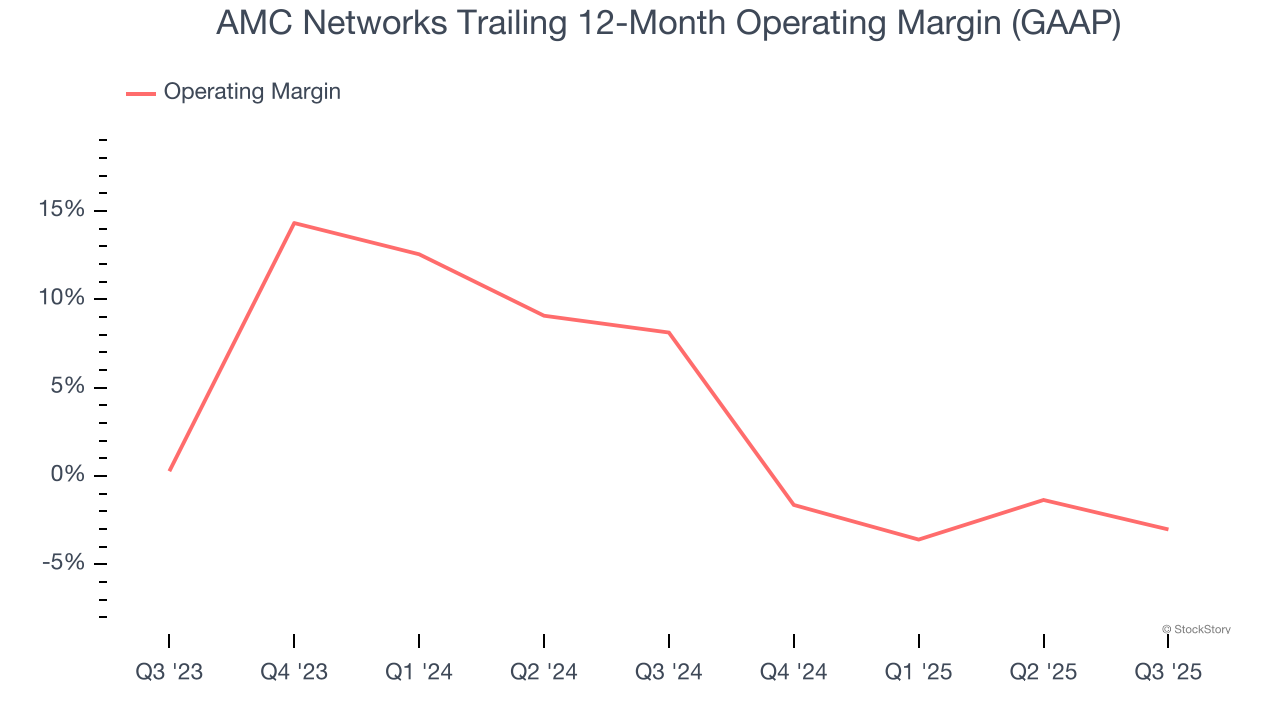

- Operating Margin: 9.9%, down from 15.6% in the same quarter last year

- Free Cash Flow Margin: 7.5%, down from 9% in the same quarter last year

- Market Capitalization: $314.5 million

Chief Executive Officer Kristin Dolan said: "Our performance in the third quarter marks a key milestone in our transition from a cable networks business to a global streaming and technology focused content company. Streaming revenue growth accelerated and will represent our largest single source of domestic revenue this year. We again delivered healthy free cash flow and remain on track to achieve our increased outlook of $250 million in free cash for the full year. We have built the components of a modern media business that is nimble, independent and well suited to today’s environment and whatever comes next."

Company Overview

Originally the joint-venture of four cable television companies, AMC Networks (NASDAQ:AMCX) is a broadcaster producing a diverse range of television shows and movies.

Revenue Growth

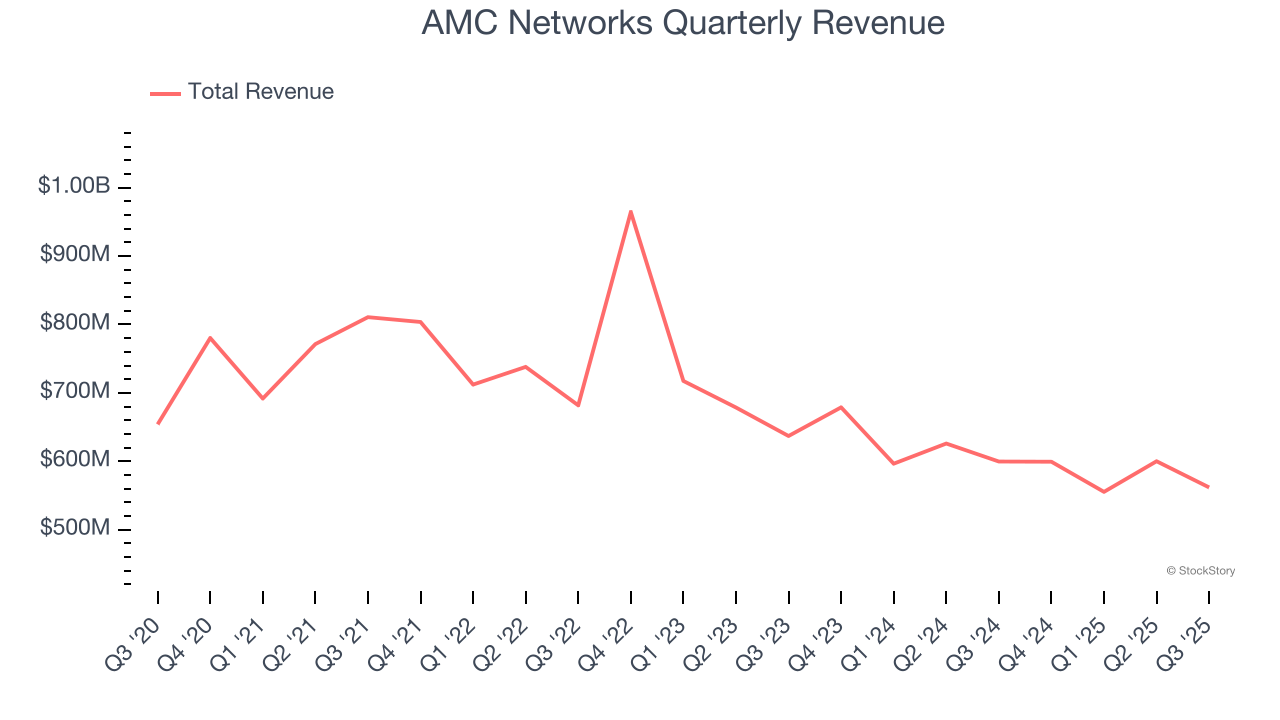

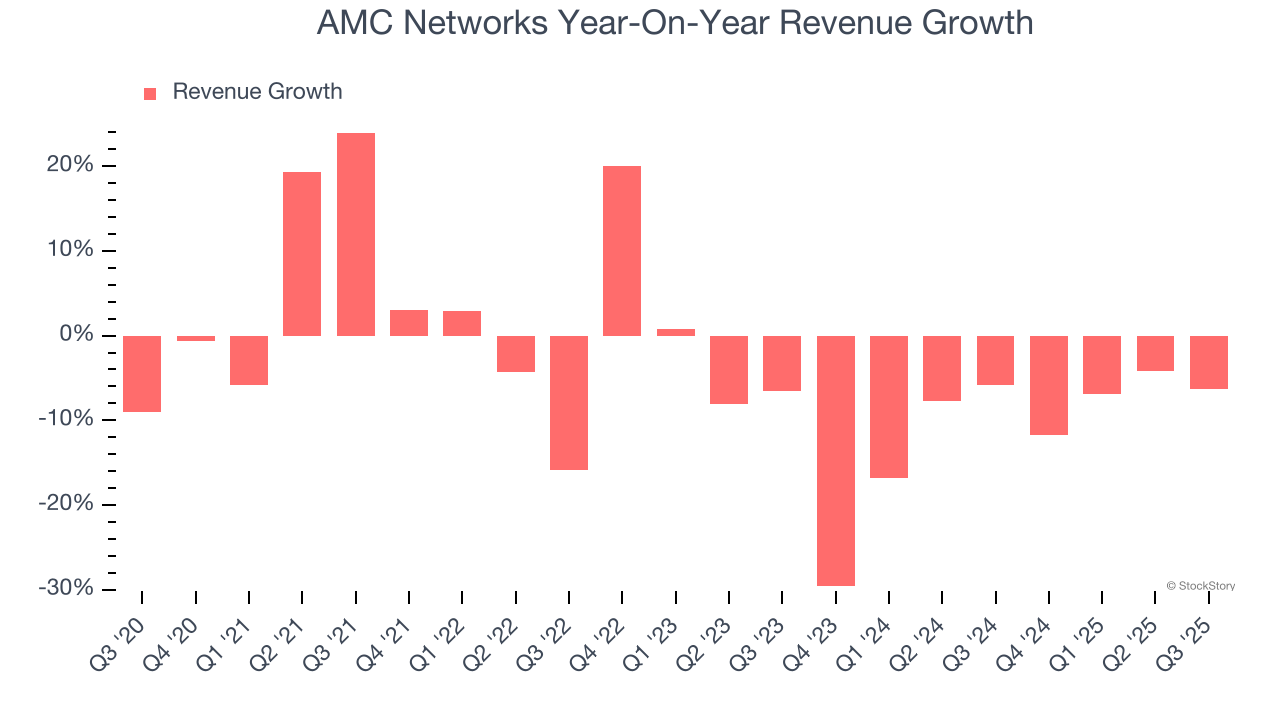

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. AMC Networks’s demand was weak over the last five years as its sales fell at a 3.9% annual rate. This wasn’t a great result and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. AMC Networks’s recent performance shows its demand remained suppressed as its revenue has declined by 12.1% annually over the last two years.

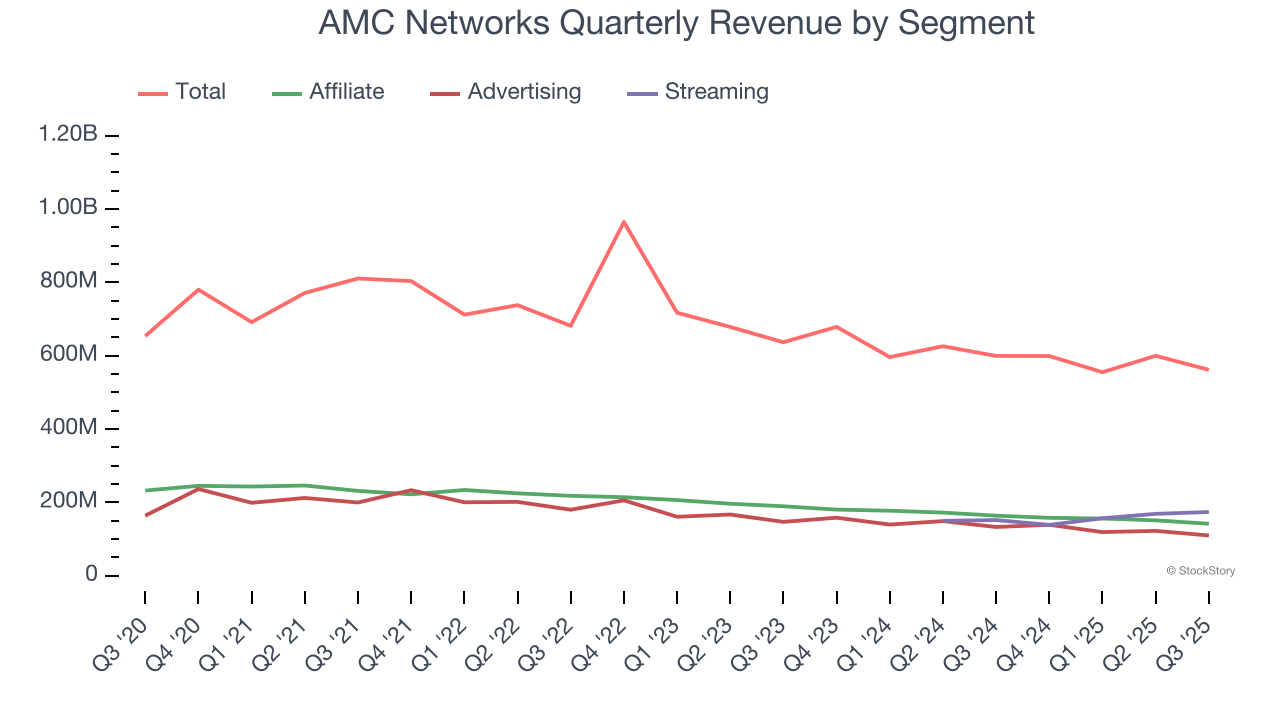

AMC Networks also breaks out the revenue for its three most important segments: Affiliate, Advertising, and Streaming, which are 25.3%, 19.6%, and 31% of revenue. Over the last two years, AMC Networks’s Affiliate (retransmission and licensing fees) and Advertising (marketing services) revenues averaged year-on-year declines of 13.2% and 14.8% while its Streaming revenue (subscription video on demand) averaged 13.6% growth.

This quarter, AMC Networks’s revenue fell by 6.3% year on year to $561.7 million but beat Wall Street’s estimates by 2.7%.

Looking ahead, sell-side analysts expect revenue to decline by 1.9% over the next 12 months. Although this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

AMC Networks’s operating margin has been trending down over the last 12 months and averaged 2.8% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, AMC Networks generated an operating margin profit margin of 9.9%, down 5.7 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

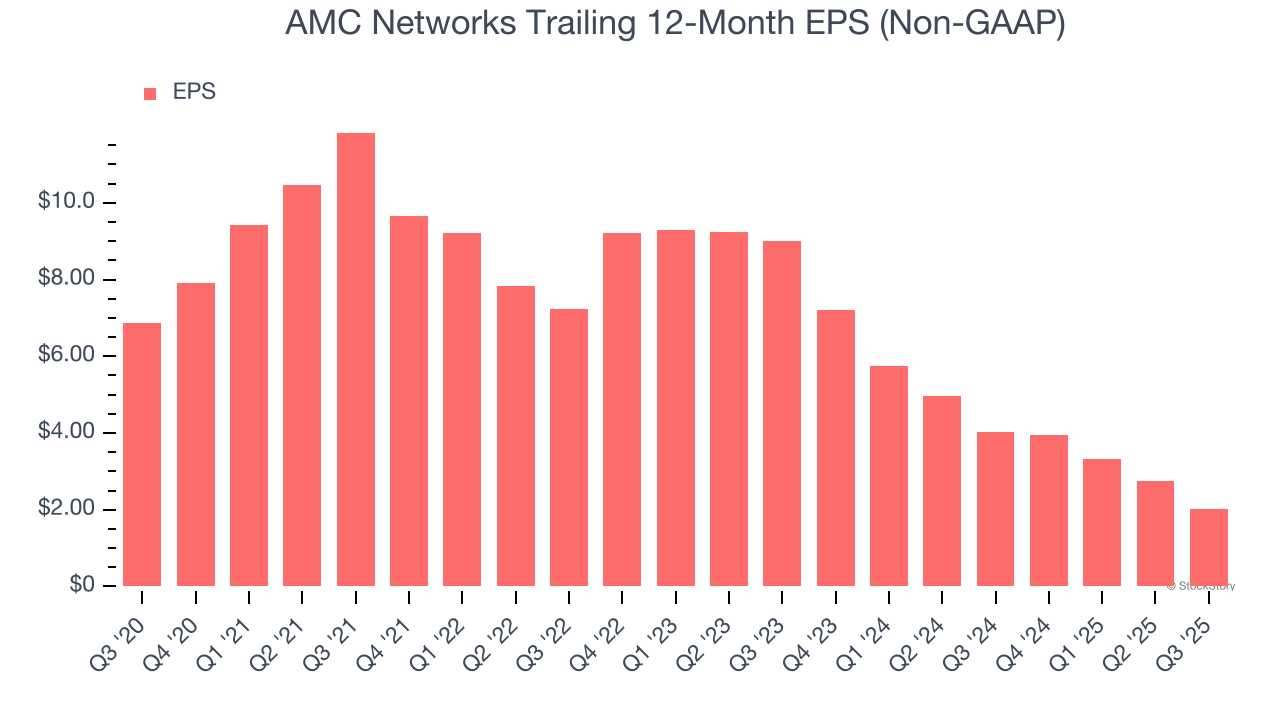

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for AMC Networks, its EPS declined by 21.6% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q3, AMC Networks reported adjusted EPS of $0.18, down from $0.91 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects AMC Networks’s full-year EPS of $2.03 to grow 15.5%.

Key Takeaways from AMC Networks’s Q3 Results

It was encouraging to see AMC Networks beat analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its Advertising revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $7.27 immediately after reporting.

Is AMC Networks an attractive investment opportunity right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.