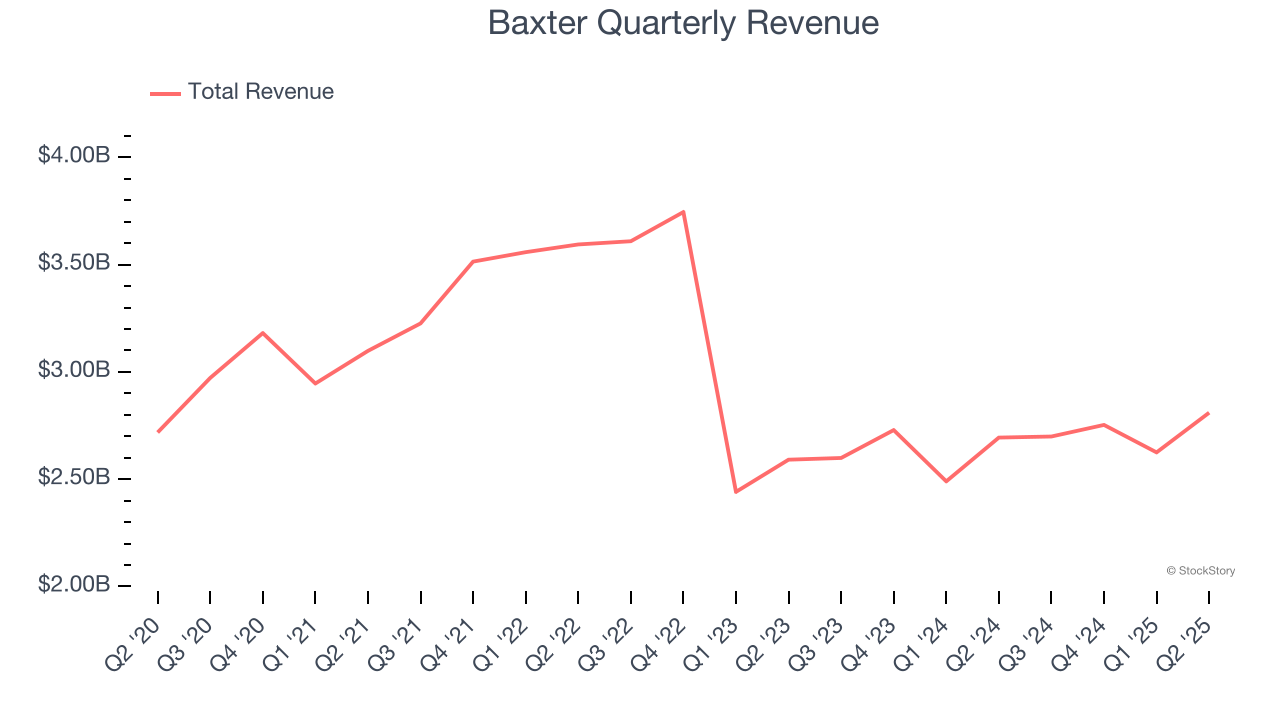

Healthcare company Baxter International (NYSE:BAX) met Wall Street’s revenue expectations in Q2 CY2025, with sales up 4.3% year on year to $2.81 billion. On the other hand, next quarter’s revenue guidance of $2.87 billion was less impressive, coming in 1% below analysts’ estimates. Its non-GAAP profit of $0.59 per share was 3.2% below analysts’ consensus estimates.

Is now the time to buy Baxter? Find out by accessing our full research report, it’s free.

Baxter (BAX) Q2 CY2025 Highlights:

- Revenue: $2.81 billion vs analyst estimates of $2.82 billion (4.3% year-on-year growth, in line)

- Adjusted EPS: $0.59 vs analyst expectations of $0.61 (3.2% miss)

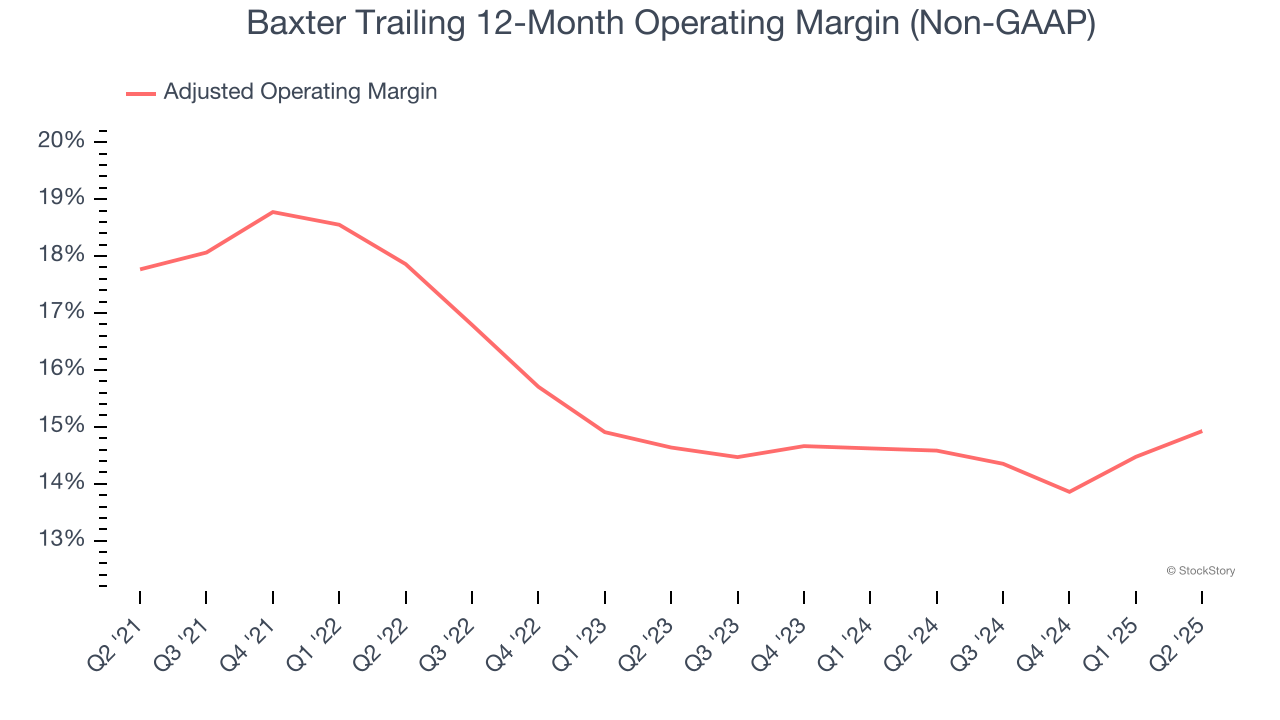

- Adjusted Operating Income: $423 million vs analyst estimates of $453.3 million (15.1% margin, 6.7% miss)

- Revenue Guidance for Q3 CY2025 is $2.87 billion at the midpoint, below analyst estimates of $2.90 billion

- Management lowered its full-year Adjusted EPS guidance to $2.47 at the midpoint, a 1.6% decrease

- Operating Margin: 6.8%, in line with the same quarter last year

- Free Cash Flow was $171 million, up from -$1 million in the same quarter last year

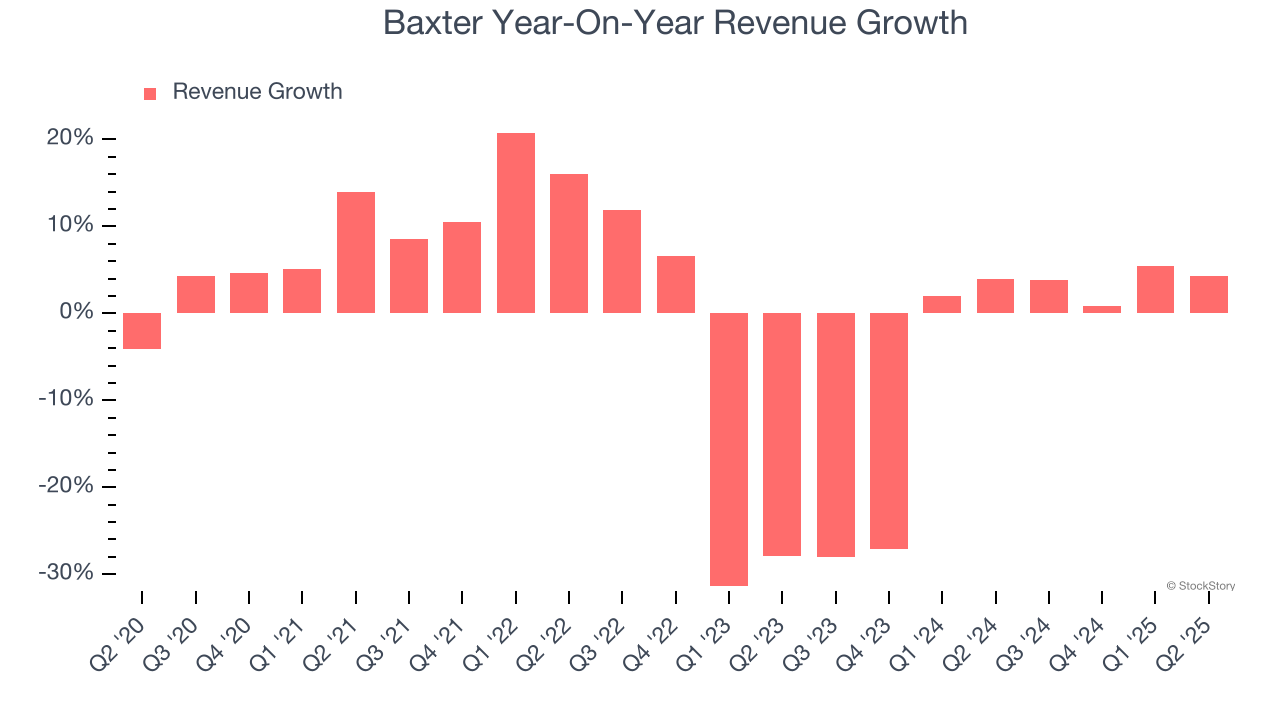

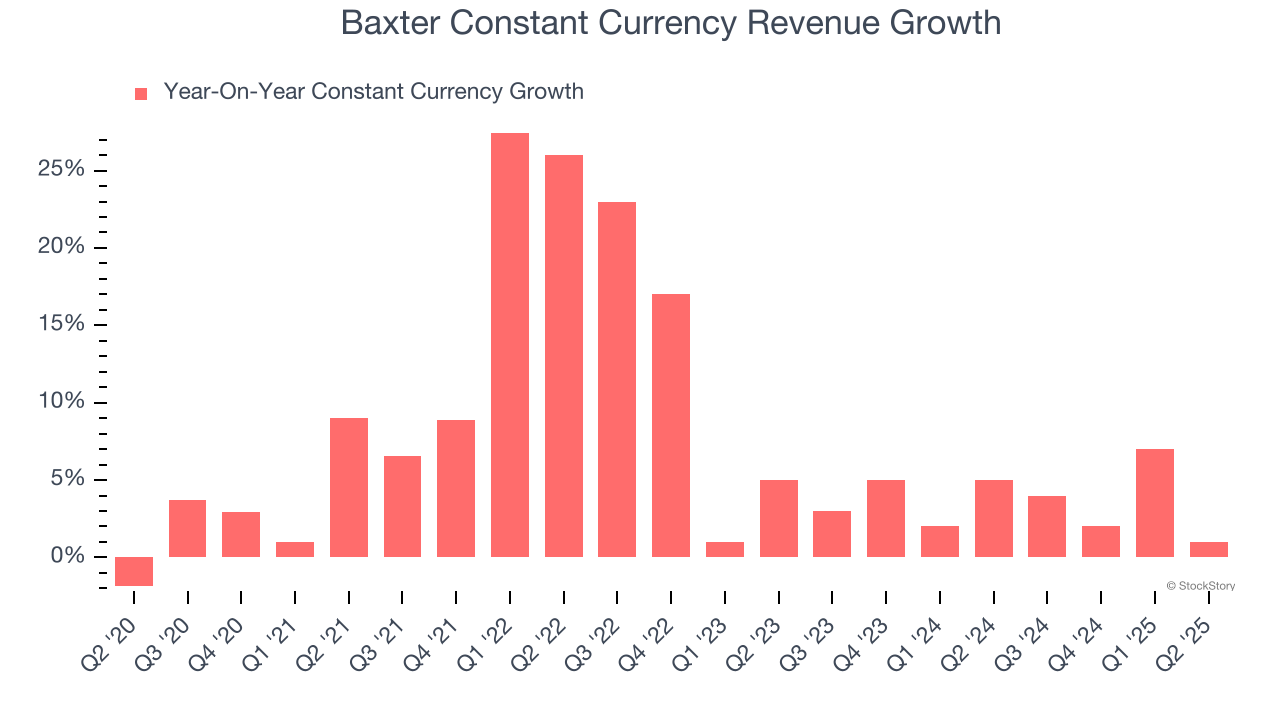

- Constant Currency Revenue rose 1% year on year (5% in the same quarter last year)

- Market Capitalization: $14.39 billion

“For the second quarter of 2025, Baxter delivered performance in line with guidance while our employees across the globe continued advancing the company’s life-sustaining Mission and building on its vision to redefine healthcare delivery,” said Brent Shafer, chair and interim CEO.

Company Overview

With a history dating back to 1931 and products used in over 100 countries, Baxter International (NYSE:BAX) provides essential healthcare products including dialysis therapies, IV solutions, infusion systems, surgical products, and patient monitoring technologies to hospitals and clinics worldwide.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Baxter struggled to consistently increase demand as its $10.89 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of poor business quality.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Baxter’s recent performance shows its demand remained suppressed as its revenue has declined by 6.2% annually over the last two years.

We can better understand the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 3.6% year-on-year growth. Because this number is better than its normal revenue growth, we can see that foreign exchange rates have been a headwind for Baxter.

This quarter, Baxter grew its revenue by 4.3% year on year, and its $2.81 billion of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 6.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.7% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and implies its newer products and services will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Baxter has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average adjusted operating margin of 16.1%.

Analyzing the trend in its profitability, Baxter’s adjusted operating margin decreased by 2.8 percentage points over the last five years. Even though its historical margin was healthy, shareholders will want to see Baxter become more profitable in the future.

This quarter, Baxter generated an adjusted operating margin profit margin of 15.1%, up 1.8 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

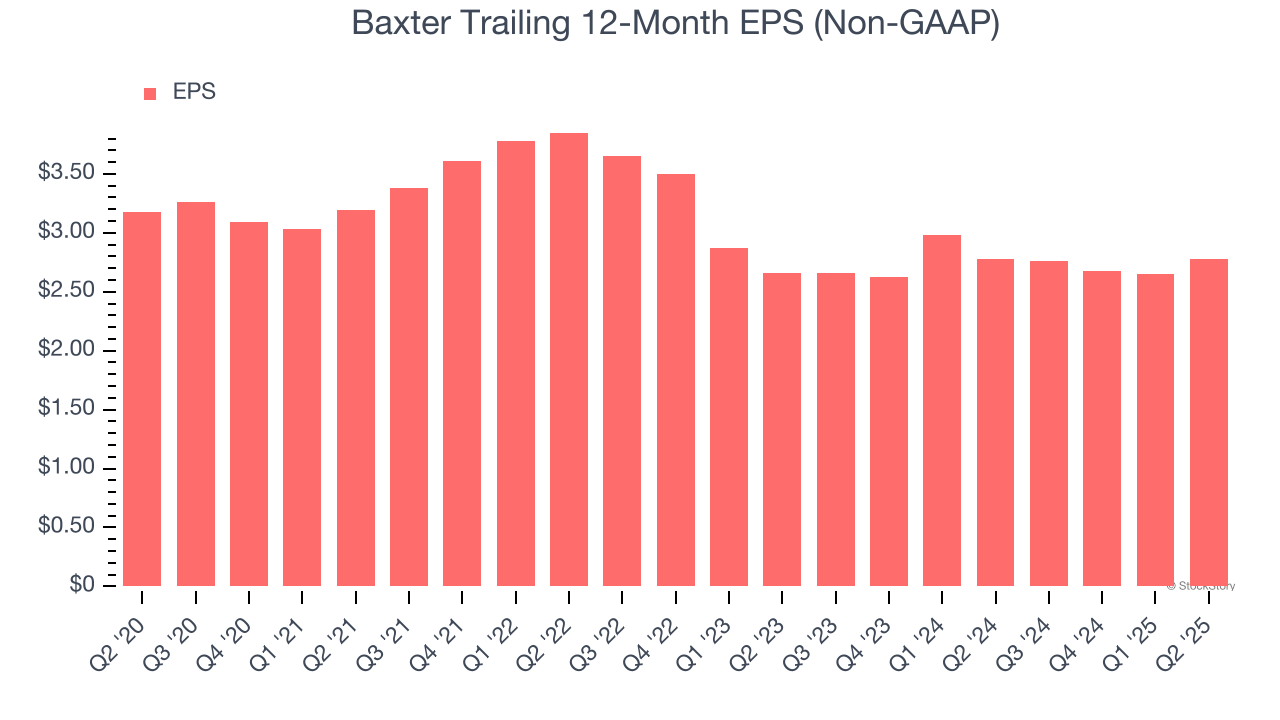

Sadly for Baxter, its EPS declined by 2.6% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences.If the tide turns unexpectedly, Baxter’s low margin of safety could leave its stock price susceptible to large downswings.

In Q2, Baxter reported adjusted EPS at $0.59, up from $0.46 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Baxter’s full-year EPS of $2.78 to shrink by 6.6%. This is unusual as its revenue and operating margin are anticipated to increase, signaling the fall likely stems from "below-the-line" items such as taxes.

Key Takeaways from Baxter’s Q2 Results

We struggled to find many positives in these results. Its EPS guidance for next quarter missed and its constant currency revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 9.2% to $25.50 immediately following the results.

Baxter’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.