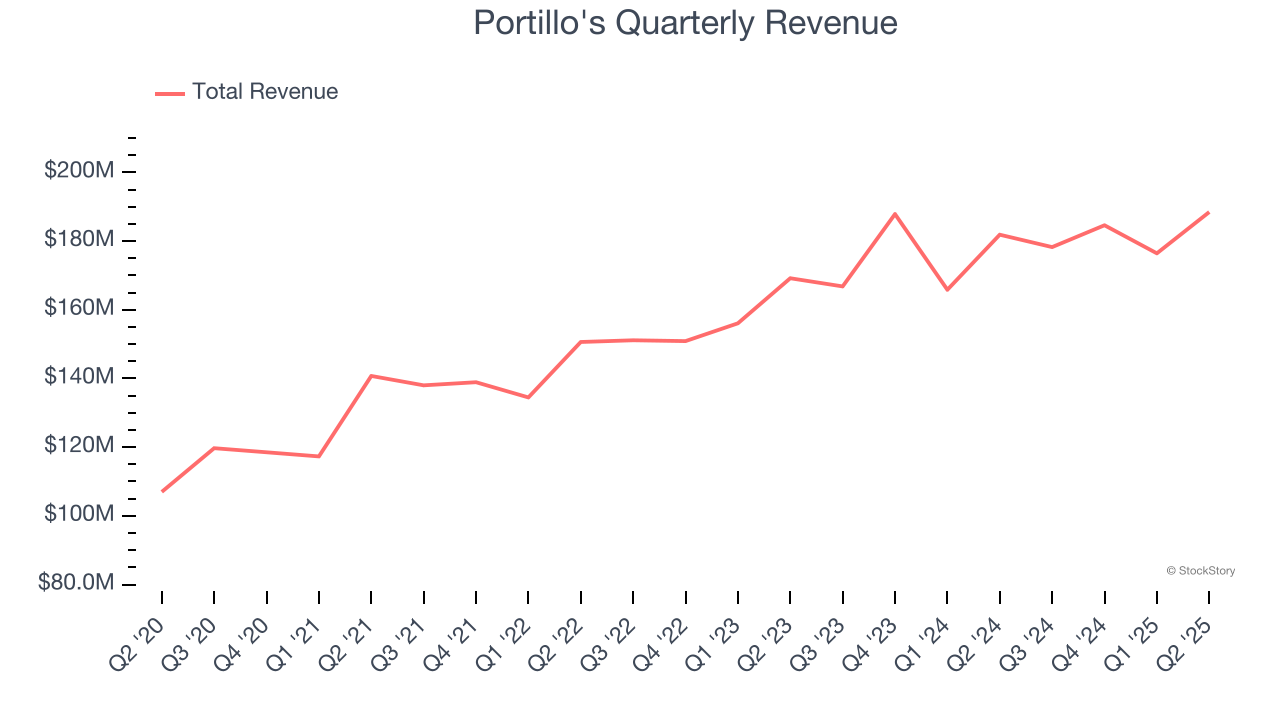

Casual restaurant chain Portillo’s (NASDAQ:PTLO) missed Wall Street’s revenue expectations in Q2 CY2025 as sales rose 3.6% year on year to $188.5 million. Its GAAP profit of $0.12 per share was in line with analysts’ consensus estimates.

Is now the time to buy Portillo's? Find out by accessing our full research report, it’s free.

Portillo's (PTLO) Q2 CY2025 Highlights:

- Revenue: $188.5 million vs analyst estimates of $196 million (3.6% year-on-year growth, 3.9% miss)

- EPS (GAAP): $0.12 vs analyst estimates of $0.11 (in line)

- Adjusted EBITDA: $30.06 million vs analyst estimates of $29.36 million (16% margin, 2.4% beat)

- Operating Margin: 9.3%, in line with the same quarter last year

- Free Cash Flow Margin: 2.8%, down from 8.6% in the same quarter last year

- Locations: 94 at quarter end, up from 86 in the same quarter last year

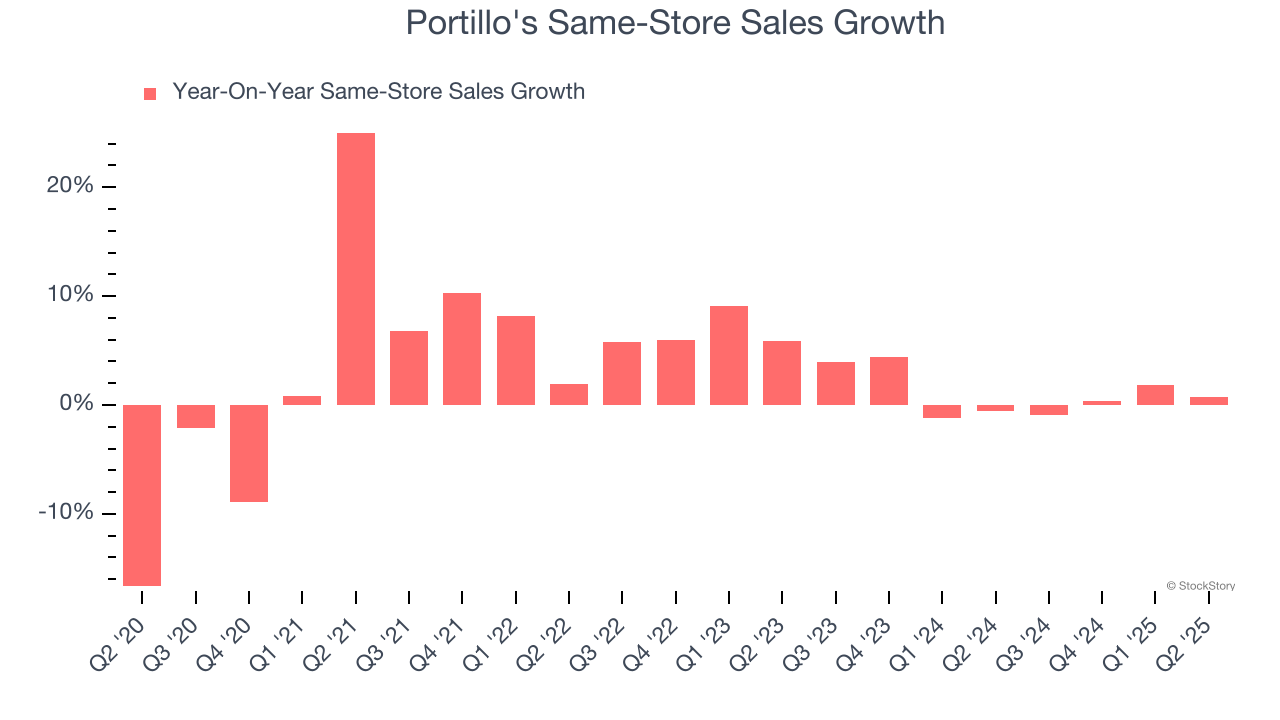

- Same-Store Sales were flat year on year (-0.6% in the same quarter last year)

- Market Capitalization: $608.1 million

“Our team operated well through a tough traffic environment in the second quarter, managing restaurant-level margins effectively and driving solid earnings,” said Michael Osanloo, President and Chief Executive Officer of Portillo’s.

Company Overview

Begun as a Chicago hot dog stand in 1963, Portillo’s (NASDAQ:PTLO) is a casual restaurant chain that serves Chicago-style hot dogs and beef sandwiches as well as fries and shakes.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $727.8 million in revenue over the past 12 months, Portillo's is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can grow faster because it has more white space to build new restaurants.

As you can see below, Portillo's grew its sales at a decent 7.8% compounded annual growth rate over the last six years (we compare to 2019 to normalize for COVID-19 impacts) as it opened new restaurants and increased sales at existing, established dining locations.

This quarter, Portillo’s revenue grew by 3.6% year on year to $188.5 million, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 14.5% over the next 12 months, an acceleration versus the last six years. This projection is healthy and implies its newer menu offerings will catalyze better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Restaurant Performance

Number of Restaurants

Portillo's sported 94 locations in the latest quarter. Over the last two years, it has opened new restaurants at a rapid clip by averaging 12.2% annual growth, among the fastest in the restaurant sector. This gives it a chance to scale into a mid-sized business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing restaurants and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Portillo’s demand within its existing dining locations has been relatively stable over the last two years but was below most restaurant chains. On average, the company’s same-store sales have grown by 1.1% per year. This performance suggests it should consider improving its foot traffic and efficiency before expanding its restaurant base.

In the latest quarter, Portillo’s year on year same-store sales were flat. This performance was a deceleration from its historical levels, showing the business is still performing well but losing a bit of steam.

Key Takeaways from Portillo’s Q2 Results

It was encouraging to see Portillo's beat analysts’ EBITDA expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. On the other hand, its revenue missed and its same-store sales fell slightly short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 12.8% to $8.28 immediately following the results.

Portillo's may have had a tough quarter, but does that actually create an opportunity to invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.