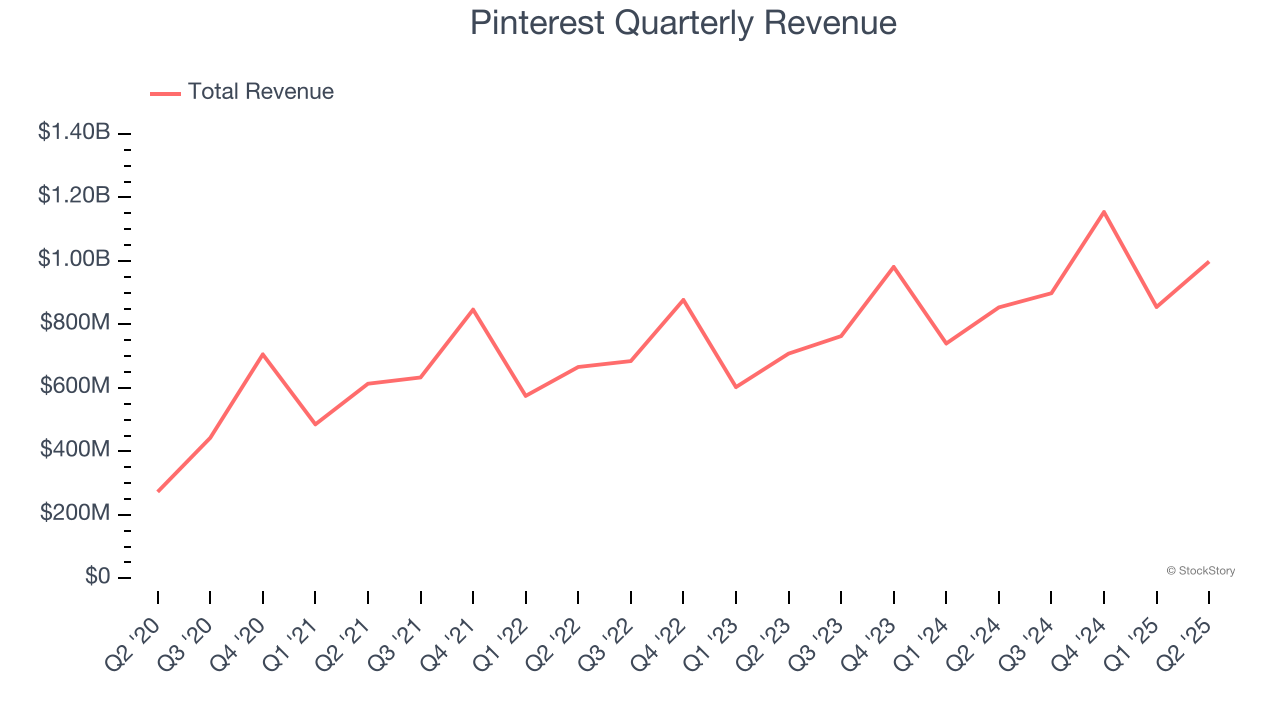

Social commerce platform Pinterest (NYSE: PINS) announced better-than-expected revenue in Q2 CY2025, with sales up 16.9% year on year to $998.2 million. Guidance for next quarter’s revenue was better than expected at $1.04 billion at the midpoint, 1.6% above analysts’ estimates. Its non-GAAP profit of $0.33 per share was 6.2% below analysts’ consensus estimates.

Is now the time to buy Pinterest? Find out by accessing our full research report, it’s free.

Pinterest (PINS) Q2 CY2025 Highlights:

- Revenue: $998.2 million vs analyst estimates of $976.4 million (16.9% year-on-year growth, 2.2% beat)

- Adjusted EPS: $0.33 vs analyst expectations of $0.35 (6.2% miss)

- Adjusted EBITDA: $250.8 million vs analyst estimates of $233.3 million (25.1% margin, 7.5% beat)

- Revenue Guidance for Q3 CY2025 is $1.04 billion at the midpoint, above analyst estimates of $1.03 billion

- EBITDA guidance for Q3 CY2025 is $292 million at the midpoint, in line with analyst expectations

- Operating Margin: -0.4%, up from -2.5% in the same quarter last year

- Free Cash Flow Margin: 19.7%, down from 41.7% in the previous quarter

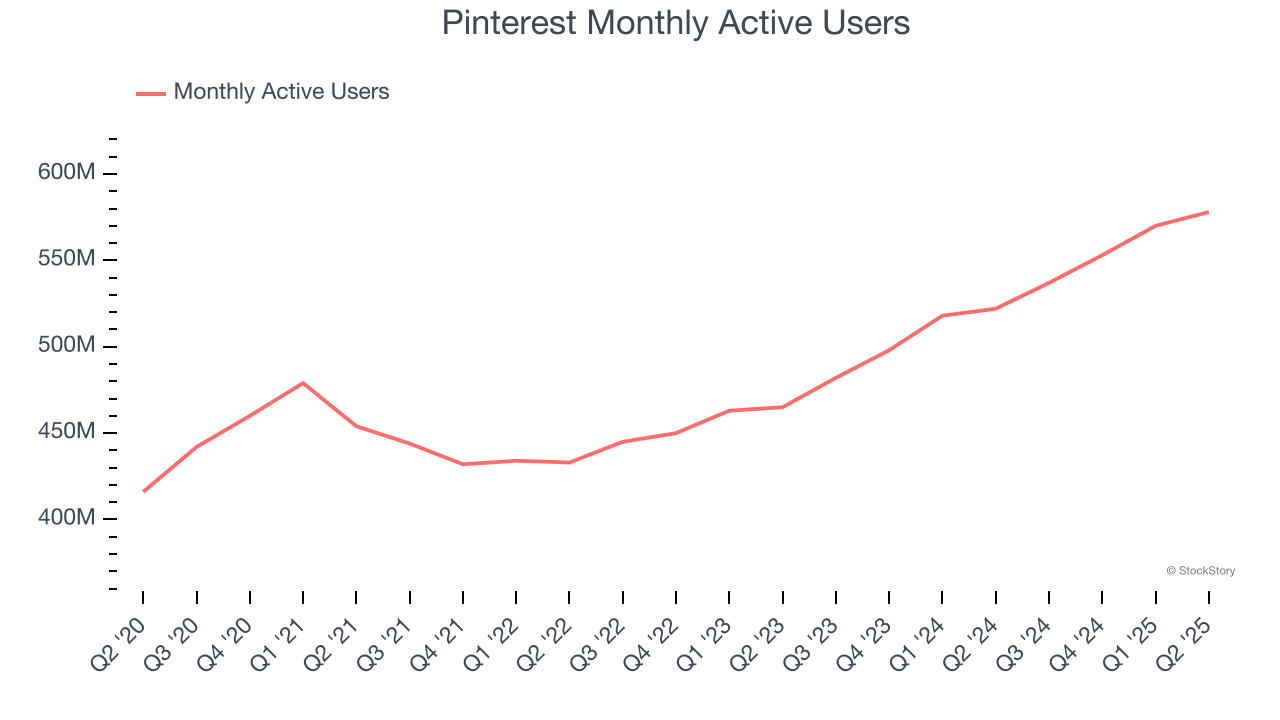

- Monthly Active Users: 578 million, up 56 million year on year

- Market Capitalization: $26.5 billion

“I’m proud of our Q2 results—delivering 17% revenue growth and another quarter of record users. We’re also excited that Gen Z has grown to over half of our user base,” said Bill Ready, CEO of Pinterest.

Company Overview

Created with the idea of virtually replacing paper catalogues, Pinterest (NYSE: PINS) is an online image and social discovery platform.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Pinterest grew its sales at a decent 12.8% compounded annual growth rate. Its growth was slightly above the average consumer internet company and shows its offerings resonate with customers.

This quarter, Pinterest reported year-on-year revenue growth of 16.9%, and its $998.2 million of revenue exceeded Wall Street’s estimates by 2.2%. Company management is currently guiding for a 16.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 14.2% over the next 12 months, similar to its three-year rate. This projection is commendable and suggests its newer products and services will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Monthly Active Users

User Growth

As a social network, Pinterest generates revenue growth by increasing its user base and charging advertisers more for the ads each user is shown.

Over the last two years, Pinterest’s monthly active users, a key performance metric for the company, increased by 10.8% annually to 578 million in the latest quarter. This growth rate is strong for a consumer internet business and indicates people love using its offerings.

In Q2, Pinterest added 56 million monthly active users, leading to 10.7% year-on-year growth. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

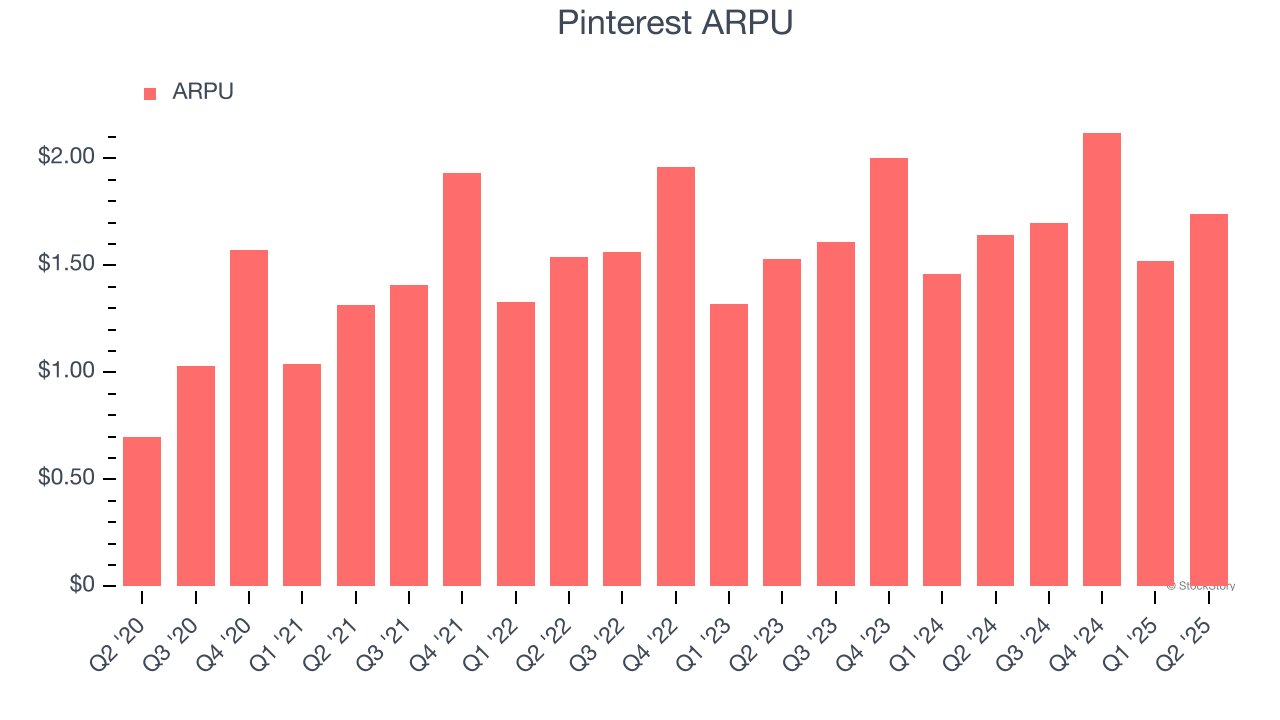

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Pinterest’s audience and its ad-targeting capabilities.

Pinterest’s ARPU growth has been decent over the last two years, averaging 5.6%. Its ability to increase monetization while effectively growing its monthly active users demonstrates the value of its platform.

This quarter, Pinterest’s ARPU clocked in at $1.74. It grew by 6.1% year on year, slower than its user growth.

Key Takeaways from Pinterest’s Q2 Results

We enjoyed seeing Pinterest beat analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter was in line. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 12.7% to $34.23 immediately after reporting.

So should you invest in Pinterest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.